Essential Findings

- The FedNow service is a revolutionary real-time payment initiative that enables 24/7 processing and settlement between financial institutions, offering faster, more secure, and more efficient transactions.

- FedNow empowers financial institutions to optimize liquidity management, reduce payment processing costs, and enjoy real-time settlement.

- Technology partners play a vital role in seamless integration with FedNow, ensuring robust security, enhancing user experience, and providing ongoing support and innovation to stay competitive.

FedNow: Overview of the Revolutionary Real-Time Payment Solution

Exciting developments in the world of payments– the FedNow Service is officially up and running!

As of July 20, 2023, the Federal Reserve made a monumental announcement: the revolutionary instant payment infrastructure has kicked off, involving 35 collaborating financial institutions, the U.S. Department of the Treasury’s Bureau of the Fiscal Service, and 16 service providers.

With the launch of the FedNow Service, enrolled U.S. banks and credit unions can swiftly and securely move funds for their customers in real time, 24/7. This advancement heralds a new era of seamless and instantaneous fund transfers. With advanced security measures, FedNow promises a secure and reliable payment experience. This real-time payment system will benefit businesses and financial institutions seeking seamless, swift, and uninterrupted payment processing, ultimately enhancing payment transactions’ overall efficiency and convenience.

Jessica Cheney, vice president of product management and digital banking solutions at Bottomline Technologies, the paytech, says: “The sheer jumps in the volume of banks that will have access to a real-time or instant payments network will lead to game-changing growth in adoption.

Several vital objectives drove the development of this real-time payment system:

- To foster competition in the banking industry by providing secure and efficient instant payment options for financial institutions, regardless of their size.

- To ensure the instant payment ecosystem’s safety, resilience, and strength.

- To encourage global interoperability, facilitating seamless transactions on an international scale.

FedNow stands out from other payment rails due to its exclusive focus on facilitating instant retail payments. Its most prominent feature is its year-round, 24/7 operation, enabling financial institutions to clear and settle retail payments instantly, even during nights and weekends.

Timeline of FedNow’s Development

- August 2018: The Federal Reserve intends to build a new real-time payment service called FedNow.

- September 2020: The Federal Reserve Board approves the development of the FedNow Service.

- January 2021: The Federal Reserve begins a pilot program for the FedNow Service, which grows into 120 participating financial institutions.

- August 2022: The Federal Reserve Bank narrows launch timing to mid-year 2023.

- July 2023: FedNow operations commence as the service goes live.

Key Components

The service enables real-time clearing and settlement of payment transactions, allowing funds to be immediately available to the recipient without pre-funding. By operating 24x7x365, the FedNow Service minimizes interbank credit risk, promoting faster and smoother payment flows.

The FedNow Service provides reporting tools offering comprehensive and real-time insights into payment transactions, allowing institutions to monitor and analyze payment flows. Reconcilement capabilities help ensure that payment records align with the expected outcomes, streamlining the process of identifying and resolving discrepancies.

Liquidity management is a crucial aspect of the FedNow Service, as it helps financial institutions optimize their cash flows and meet their liquidity needs effectively. With instant payment capabilities, financial institutions may experience more frequent fluctuations in their cash positions. The FedNow Service offers tools and mechanisms for institutions to manage liquidity efficiently, allowing them to allocate funds strategically and maintain sufficient reserves for smooth payment processing.

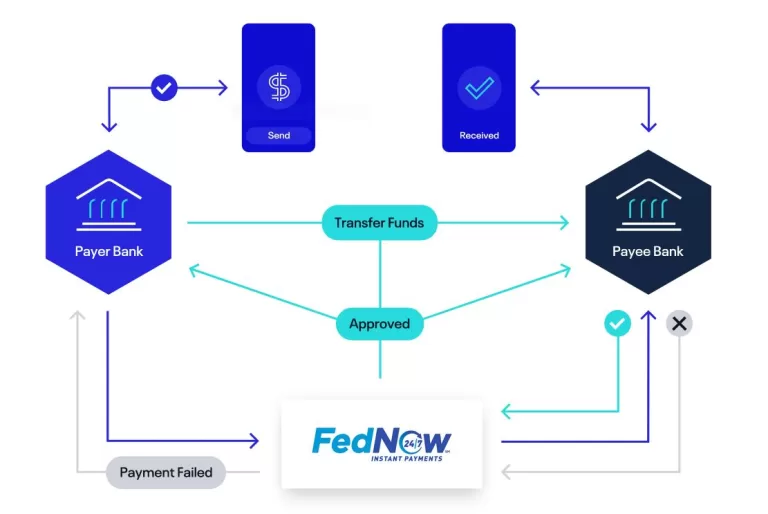

Overview of the FedNow Service Process

Image courtesy: https://www.aciworldwide.com/fednow

The general process of the FedNow Service involves the payer initiating a payment through their financial institution via an end-user interface. Once the payer’s financial institution verifies sufficient funds, it submits the payment message to the FedNow Service. The service validates the message and forwards it to the payee’s financial institution for acceptance or rejection. Upon receiving a response, the FedNow Service either deducts funds and completes the transaction or notifies the payer’s financial institution of payment failure. Once the transaction is successful, all parties are notified.

How will Financial Institutions Benefit from the FedNow Service?

The FedNow Service aims to:

- Increase inclusivity by making instant payment technology accessible to smaller community banks, ensuring equitable access for all businesses.

- Lower payment processing costs for banks and non-bank financial institutions, contributing to overall cost efficiency.

- Enable businesses to optimize cash flow management by providing immediate access to payroll processing and enabling seamless electronic fund transfers.

- Optimize liquidity management and cash flow forecasting for businesses, helping them manage expenses and maintain positive vendor relationships.

- Strengthen security by establishing industry-wide standards for disputing fraudulent transfers, promoting ISO 20022 conformity, and implementing secure payment authentication methods.

Comparing FedNow Service with Other Payment Systems: What Sets It Apart!

Feature

| FedNow Service | Other payment systems |

Transaction Type | Directly between bank accounts, completed in seconds. | Some require holding balances in the app, while others involve delayed bank-to-bank transfers. |

Applicability | All types of payments, including between businesses and consumers. | Mostly for person-to-person payments |

Speed of Transactions | Near-instantaneous transactions between financial institutions | Varies, with some systems taking longer to process transactions. |

Availability | Available 24/7/365 | Operating time may be limited (business hours) for some systems |

Transaction Limits | Higher transaction limits | Limits may vary among different payment systems |

Processing Times and Fees | Faster processing times and lower fees | Longer processing time and higher transaction fees in some systems |

Credit Risk` | Reduced credit risk due to real-time settlement | Increased credit risk due to delay in settlement |

ACH Processing | Faster and instantaneous transfers | ACH involves a longer processing time |

Credit card transactions | Faster processing time and lower fees | The transaction may take several days and incur higher fees |

Digital wallets (e.g.,PayPal, Venmo) | Faster and more cost-effective transactions | Digital wallets may have longer transfer times and higher fees for instant transfers. |

Potential challenges in implementing

- Technical Integration: Financial institutions may need help integrating their systems with the FedNow infrastructure. Integration requires significant time and resources, including upgrades to existing technology and collaboration with third-party providers.

- Costs and Investment: Upgrading systems to support real-time payments might require significant financial investment.

- Compliance and Regulations: Adhering to regulatory requirements and compliance standards can take time for financial institutions.

- Scaling for Demand: As usage of the FedNow service grows, scaling the infrastructure to handle increased transaction volumes will be crucial.

The role of technology partners’ involvement in preparing for FedNow

As the FedNow Service continues to gain traction and expand its reach, financial institutions should embrace this transformational technology to stay ahead in the market. Financial Institutions can significantly benefit from the support and expertise of their core technology partners.

Here are five key roles these partners should play in helping financial institutions prepare for the FedNow Service:

- Technological Integration: Core banking partners ensure smooth integration of banks’ systems with FedNow, facilitating real-time payment processing.

- Security and Fraud Prevention: Implement robust security measures and offer advanced authentication and monitoring systems to protect against threats.

- Compliance and Regulatory Support: Partners help banks navigate complex regulatory requirements, ensuring compliance and avoiding penalties.

- User Experience and Customer Education: Partners improve user experience with intuitive interfaces and assist in educating customers about instant payments.

- Ongoing Support and Innovation: Provide continuous support, updates, and innovative solutions to stay ahead in the dynamic financial landscape.

Implications for future

ACI Worldwide recently announced that the introduction of FedNow is a significant growth catalyst for instant payments. Their projections anticipate that real-time transactions in North America will increase from 3.9 billion in 2022 to 13 billion by 2027, reflecting a compound annual growth rate of 27.3%.

The introduction of FedNow marks a transformative milestone for the U.S. payments industry, representing the most significant development from the Fed in decades. This innovative service opens numerous opportunities for financial institutions. However, their ability to harness its potential will hinge on their preparedness to adopt real-time payments and the associated cost considerations for participation. With projections pointing towards an exponential surge in real-time transactions, financial institutions have a unique opportunity to ride this tide of change and shape the future of payments. Embracing FedNow isn’t just about keeping up; it’s about harnessing the power of immediacy, security, and efficiency to reshape how commerce flows.

FedNow FAQs

Will FedNow replace cash?

No. The FedNow system will not substitute the dollar, nor will it replace digital currency.

Will FedNow create a digital currency?

FedNow is not related to a digital currency.

Will FedNow dominate the Global Payment System?

FedNow’s influence on the worldwide money transfer system among banks will be substantial in the foreseeable future. However, the comprehensive testing and adoption of the platform by financial institutions will necessitate several years.

Will there be a FedNow app?

No FedNow app exists. The Federal Reserve doesn’t serve consumers and businesses directly with payment services. Banks and credit unions can offer instant payments through updated interfaces like mobile apps and websites.

Does the Fed have access to my bank account with the FedNow Service?

No. The Federal Reserve and the FedNow Service cannot access individuals’ bank accounts or control how they spend their money.

Discover more insights on various topics in our Blogs.

Get Insights to stay ahead in the Lending Industry.

Insights delivered monthly!