Understand today’s prevalent digital payment systems and emerging fraud tactics targeting them. Explore techniques CPAs use for fraud detection and best practices to protect clients as payment technologies and risks evolve.

Category: Blog

Efficient Loan Origination: Fueling Community Bank Growth

Understand today’s prevalent digital payment systems and emerging fraud tactics targeting them. Explore techniques CPAs use for fraud detection and best practices to protect clients as payment technologies and risks evolve.

In this conversation with JP James, CEO of Hive, a financial services firm based in Atlanta, we discussed what it means to lead a fintech company in 2023 and the future of consumer lending.

Summary

JP begins by sharing how he was inspired by the ideas of Ray Kurzweil, who discussed the future of humanity and technology. Learn how Hive has been working towards its vision of leveraging cutting-edge technology to create a scalable impact in the financial services space and support people left behind by the banking sector. He mentions that their success metrics are not solely financial, and instead, aimed to create scalable impact and bridge gaps during crises for consumers in various regions, including the US, Latin America, Southeast Asia, and eventually Africa.

Next, hear about how the partnership between Hive and Insight Consultants has brought together the worlds of financial and technology services, creating a robust and integrated ecosystem. The success of the collaboration is attributed to a shared value system, high standards, and a culture of constant experimentation and innovation.

Regarding the challenges and opportunities in the consumer lending space, JP highlights that consumer lending is certainly here to stay and there is evidence of a growing demand for it. He sees regulatory environments as an opportunity rather than a hindrance, enabling players to function with more clarity.

Lastly, when asked for advice for aspiring CEOs in the fintech space, JP speaks about the role of leadership and mentoring. Preferring the title of “coach” rather than “CEO”, he believes in servant leadership and emphasizes the need for adaptability, willingness to learn, and making data-driven decisions.

JP James, CEO - Hive

Key Takeaways

- BNPL’s rapid growth draws regulatory focus on financial compliance, safeguarding consumer rights, privacy, and economic well-being.

- BNPL regulations differ by country; focus includes transparency, responsible lending, credit assessments, data privacy, and anti-money laundering.

- BNPL providers must expect upcoming regulations, engage in dialogue, enhance compliance, and adapt to diverse frameworks for successful navigation.

Growing concerns and need for regulatory compliance in BNPL space

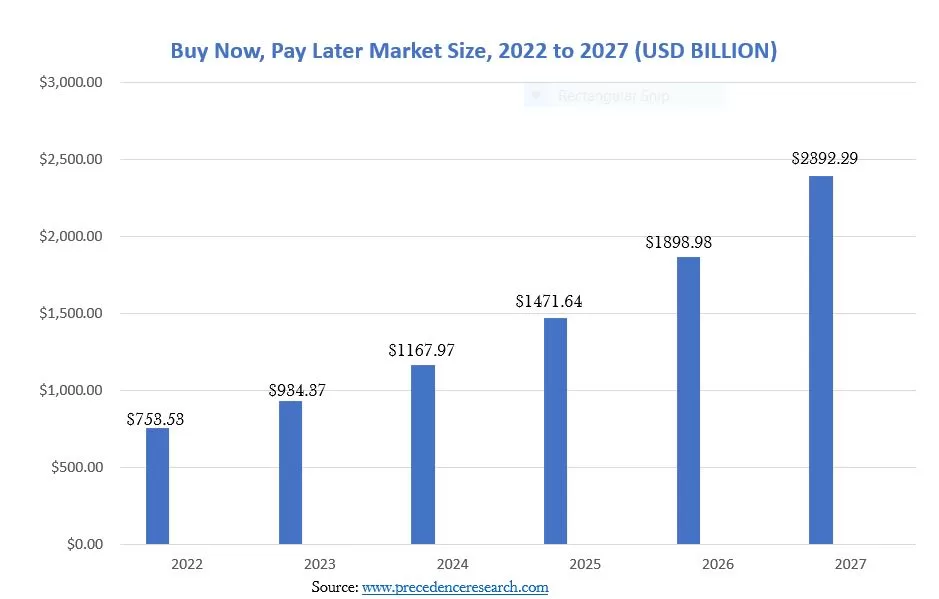

The BNPL industry has significantly expanded from 2019 to 2021. There was an astonishing 970% surge in the loans issued by BNPL lenders. Also, BNPL users quadruple.

Buy Now Pay Later (BNPL) has experienced an explosive surge in popularity thanks to its convenience, absence of interest rates, and streamlined approval process. Nevertheless, as BNPL gains traction, the importance of financial compliance within the industry has grown. With more consumers embracing this payment option, there is a pressing need to ensure adequate measures are in place to protect consumer rights, privacy, and financial well-being. As a result, regulators increasingly focus on establishing guidelines and standards to address transparency, fair lending practices, responsible lending, and anti-money laundering measures in the BNPL space. Striking the right balance between innovation and regulation is essential to foster consumer trust, maintain financial stability, and promote sustainable growth in this evolving sector. Overall, BNPL’s popularity calls for a cautious approach that prioritizes both customer convenience and protection.

Regulatory Landscape of the BNPL Industry

In virtually every country where Buy Now, Pay Later is offered as a payment method, it is commonly observed that BNPL is excluded from local laws and regulations.

As fintech businesses increasingly adopt Buy Now, Pay Later (BNPL) models, staying abreast of the latest BNPL regulatory changes and requirements becomes paramount. However, the regulatory landscape for BNPL varies across countries, with each area adopting its approach to address the unique challenges associated with these services. The Consumer Financial Protection Bureau (CFPB) has taken the lead in spearheading BNPL regulation in the United States.

Acknowledging the inherent risks associated with BNPL as a financing solution, the CFPB recently conducted a study highlighting the dangers consumers may encounter, including debt accumulation, overextension, and unauthorized harvesting of user data by BNPL providers. As a result of these findings, the specifics of forthcoming regulations are still unknown; however, industry experts anticipate the CFPB will soon unveil proposed rules. In an effort to address these concerns, anticipated regulations aim to align BNPL within the existing regulatory framework governing traditional credit companies, imposing comparable guidelines and restrictions on BNPL providers. This move comes as a means to protect consumers and ensure responsible lending practices across the industry.

Key Areas of Regulatory Scrutiny

Disclosure and Transparency

Responsible Lending Practices

Credit Assessments and Underwriting

Data Privacy and Security

Anti-Money Laundering (AML) and Fraud Prevention

Disclosure and Transparency

Regulators closely examine the clarity and adequacy of disclosures provided by BNPL providers. The aim is to ensure consumers understand their financial obligations and the costs of using BNPL services.

Responsible Lending Practices

Regulators stress responsible lending in the BNPL industry, focusing on affordability assessments and consumer protection.

Credit Assessments and Underwriting

Scrutinize credit assessment and underwriting in the BNPL sector, evaluating accuracy, suitability, and risk management practices.

Data Privacy and Security

BNPL providers are expected to comply with relevant data protection regulations, implement robust data security measures, and ensure proper consent and transparency regarding the use of customer data.

Anti-Money Laundering (AML) and Fraud Prevention

Focus on verifying customer identities, monitoring transactions for suspicious activity, and implementing measures to mitigate the risk of fraud and money laundering.

Future Ahead: Challenges to Face and Actions to Take by BNPL Providers

Until now, small, emerging fintech companies have dominated the BNPL space, managing to avoid substantial regulatory scrutiny. However, this landscape is on the brink of transformation. Despite the absence of concrete regulations thus far, which has facilitated the growth of the BNPL industry, a transitional phase is imminent. Consequently, BNPL service providers will soon face the realization of navigating a market governed by diverse regulatory regimes and varying operational approaches. In light of this upcoming shift, heightened awareness of the complexities involved in complying with regulations and adapting to different regulatory frameworks will become essential.

Major challenges

Regulators increase scrutiny

The federal financial regulatory agencies, including the CFPB, strongly focus on consumer protection. As a result, these regulatory efforts demand heightened compliance measures, stricter adherence to responsible lending practices, and robust consumer protection policies. BNPL providers must proactively invest resources and expertise to meet evolving regulatory requirements. This includes navigating complex compliance frameworks and addressing potential gaps or vulnerabilities. By doing so, BNPL companies can ensure they align with the regulatory landscape while maintaining a commitment to safeguarding consumer interests.

Increased Competition

BNPL providers struggle to differentiate in a crowded market where digital upstarts and legacy players launch new products and forge partnerships.

Banking Partners Turning Cautious

If default trends are unfavorable, they may be looking to de-risk their relationships with BNPL providers and reevaluate their role in the BNPL segment. This can result in stricter lending criteria, reduced funding opportunities, or even reconsidering their involvement in the BNPL segment altogether.

Bureau Reporting wake-up call

With major credit reporting agencies incorporating BNPL data into credit reports, the potential credit impacts of delinquent BNPL loans will become more visible to lenders and financial institutions. As a result, this heightened visibility can influence consumer behaviors, as individuals may become more cautious about their BNPL usage and repayment habits to avoid negative credit report impacts. Consequently, BNPL providers may experience a shift in customer behavior, with users adopting more responsible borrowing practices. Moreover, this increased visibility may subject BNPL providers to greater scrutiny from lenders and financial institutions with access to additional data points to assess borrowers’ creditworthiness. As a potential consequence, BNPL providers may also face the challenge of managing potentially higher default rates, prompting them to prioritize responsible lending and risk assessment strategies further.

Act now to tackle challenges

- Establish a comprehensive compliance framework aligned with regulatory requirements. This includes implementing policies, procedures, and internal controls that ensure adherence to consumer protection laws, responsible lending practices, and data privacy regulations.

- Differentiate themselves by focusing on innovative product offerings, enhancing customer experience through personalized services, and fostering strategic partnerships to expand their market reach and stand out in the crowded BNPL landscape.

- Create a regulatory strategy that allows for the growth of your risk management and compliance programs as your BNPL portfolio grows. Strengthen affordability assessments to evaluate a consumer’s loan repayment ability accurately. Consider income verification, creditworthiness checks, and other relevant factors to mitigate over-indebtedness risk.

- Prioritize responsible lending practices, implement robust credit risk assessment processes, and offer customers proactive financial education and support.

Proactive Compliance is Key for BNPL Players

While there’s no specific BNPL regulation today, there are frameworks both at the federal and state level for consumer-facing products that can be used to examine and enforce companies offering BNPL products. As a result, compliance and legal teams should be proactive and build out processes now to prepare for inevitable BNPL regulation and get out ahead of regulatory scrutiny.

Moving forward, Buy Now, Pay Later greatly appeals to merchants and consumers as a payment method. However, as the concept evolves and technology advances in the future, the BNPL industry is expected to experience continued growth. Nevertheless, the primary emphasis will now shift towards maintaining compliance with regulatory requirements and prioritizing delivering fair and transparent products that benefit consumers. In doing so, BNPL providers can position themselves for long-term success while fostering trust and confidence among their customer base. By adapting to changing regulatory landscapes and focusing on consumer well-being, the BNPL industry can thrive in an increasingly regulated financial market.

Get Insights to stay ahead in the Lending Industry.

Insights delivered monthly!

In the ever-evolving landscape of the lending industry, compliance has emerged as a vital cornerstone for success. With its complex regulatory framework and stringent requirements, the financial services sector emphasizes maintaining compliance standards. For lenders, adherence to regulatory guidelines and industry best practices is not merely a legal obligation but a strategic imperative. It ensures the integrity of their operations, builds trust with customers and stakeholders, and safeguards against reputational risks and costly penalties.

In this article, we delve into the top compliance challenges facing the financial services industry, shedding light on the importance of compliance and its profound impact on the lending landscape.

Top 5 Compliance Challenges

The financial services industry faces the daunting task of constantly changing regulations, such as new data privacy laws, environmental regulations, and anti-money laundering measures. Financial institutions, including smaller ones, must allocate resources to ensure compliance, often straining their budgets.

Managing cybersecurity risks in the financial industry is challenging due to the increasing sophistication of cyber threats and the evolving regulatory landscape. Financial organizations must invest in robust cybersecurity measures, which can be resource intensive. Additionally, staying updated with compliance requirements and adapting security measures accordingly is crucial. Fostering a culture of security awareness among employees further adds complexity to maintaining effective cybersecurity practices.

The cost of neglecting cybersecuirty risks include

- Financial losses from data breaches and theft

- Reputational damage and loss of customer trust

- Legal and regulatory consequences for non-compliance

- Operational disruptions and downtime

- Intellectual property theft and compromise

- Negative impact on employee morale

- Customer loss and decreased loyalty

Organizations must prioritize cybersecurity and implement robust measures to protect their data, systems, and reputation to avoid these costs.

The growing emphasis on data privacy, fueled by regulations like the General Data Protection Regulation (GDPR) and California Consumer Privacy Act (CCPA), necessitates stringent data governance practices and mechanisms to safeguard customer information. Ensuring overall privacy and data security can be challenging as cyber threats evolve and become more sophisticated.

Measures to Protect Data Privacy and Compliance

- Implement strong data security measures such as encryption, firewalls, and access controls.

- Develop and enforce clear data privacy policies and regularly train employees on their responsibilities.

- Conduct regular data privacy assessments to identify and address vulnerabilities.

- Obtain explicit consent and provide transparency on how personal data is used.

- Keep security systems and software up to date to address vulnerabilities.

- Train employees on data privacy best practices and promote a culture of privacy awareness.

- Establish an incident response and data breach notification procedures.

- Choose trusted service providers with strong data privacy practices.

Environmental, Social, and Governance (ESG) considerations are gaining prominence, requiring financial institutions to integrate sustainability principles into their operations, disclosures, and risk management frameworks to meet evolving ESG compliance requirements. Financial institutions must also consider social factors such as diversity, inclusion, and community impact in decision-making. Additionally, effective governance practices entail transparent reporting, ethical conduct, and risk management aligned with ESG standards. Meeting evolving ESG compliance requirements involves developing policies, frameworks, and reporting mechanisms to ensure alignment with sustainability goals and meet the expectations of regulators, investors, and stakeholders.

Indeed, the need for more talent in the compliance sector is a significant challenge. The demand for skilled compliance professionals has been increasing due to the growing complexity of regulations and the need for organizations to ensure compliance. However, finding and retaining qualified individuals with the necessary expertise in compliance and regulatory matters can take time and effort. This talent shortage creates a competitive landscape for organizations seeking to fill compliance roles and poses a risk in maintaining effective compliance programs. Organizations must invest in talent development, recruitment strategies, and training initiatives to address this challenge and build a capable compliance workforce.

Steps to alleviate compliance challenges

- Embrace Technology for Agile Compliance: Embrace advanced software solutions that automate compliance processes, enabling your organization to stay updated with evolving regulations. Implement real-time monitoring, data analytics, and machine learning algorithms to identify and adapt to regulatory changes promptly.

- Enhance Risk and Compliance Measures: Utilize technology-powered risk assessment and management tools to identify, assess, and prioritize risks across your organization. Leverage data analytics, machine learning, and artificial intelligence to analyze data and gain valuable insights for effective risk mitigation strategies.

- Implement Robust Compliance Monitoring: Establish robust monitoring mechanisms to identify and address compliance issues proactively. Leverage technology to automate monitoring processes, ensuring timely detection of any compliance deviations. Maintain accurate records and generate comprehensive reports to demonstrate compliance with regulatory authorities.

- Conduct Regular Compliance Reviews: Schedule periodic reviews and assessments of your compliance program to identify gaps or areas requiring enhancement. Utilize technology to streamline review processes, track progress, and implement necessary adjustments to strengthen compliance measures.

Ensuring compliance for sustainable success

Compliance has become a critical aspect of success in the lending industry. Financial institutions must navigate a complex regulatory landscape to maintain integrity and protect their customers and stakeholders. By embracing technology, enhancing risk and compliance measures, implementing robust monitoring, and conducting regular reviews, lenders can strengthen their compliance efforts and stay ahead of evolving regulations.

Contact Us if you want to learn more about how our technology services can help your compliance management.

Get Insights to stay ahead in the Lending Industry.

Insights delivered monthly!

The adoption of digital onboarding represents a paradigm shift in the lending industry. Lenders leveraging technological advancements can streamline onboarding, enhance customer satisfaction, and drive operational efficiency. Lenders can demonstrate their commitment to providing a modern and customer-centric experience, setting themselves apart from competitors.

Weighing the Options: Onboarding Solutions and Their Pros and Cons

Electronic Signature Solutions

An integral part of a fully digital onboarding process is the implementation of electronic signatures secured with OTP (One-Time Password). With this approach, customers can seamlessly complete the onboarding flow online. The system generates the necessary documents for signature, which can be instantly reviewed in real-time or downloaded for future reference. This ensures a secure and efficient onboarding experience, eliminating the need for physical paperwork.

Click here to explore the top Electronic Signature Softwares.

Pros

Cons

Pros

- Electronic signature solutions enable lenders to obtain legally binding signatures electronically, eliminating the need for physical paperwork.

- They offer convenience and speed and enhance the overall customer experience.

Cons

- Some customers may still need clarification about the security and validity of electronic signatures.

- Ensuring compliance with relevant regulations and addressing data privacy and security concerns is essential.

Identity Verification Solutions

Digital identity verification services use advanced technologies, such as facial recognition, document verification, and biometric authentication, to confirm the customer’s identity. Users typically provide their personal information and submit supporting documents online. The service then analyzes the data and documents to authenticate the user’s identity, comparing it against various trusted data sources and verification checks to ensure accuracy and detect potential fraud.

Leading Identity Verification Software: Learn more

Pros

Cons

Pros

- This solution utilizes advanced techniques to verify identities, reducing the risk of fraud and identity theft.

- Automated verification processes streamline onboarding, reducing manual effort, paperwork, and associated costs while accelerating customer onboarding or user authentication.

- Users can undergo identity verification remotely, eliminating the need for physical presence and enabling seamless onboarding or account access from anywhere.

Cons

- The accuracy of identity verification services may vary, and false positives or negatives can occur.

- Collecting and processing personal data for verification raises privacy and security concerns.

- Digital identity verification relies on technology infrastructure, internet access, and user familiarity with digital processes. This may pose challenges for individuals who need more of these

Digital Document Management Solutions

A digital document management solution is a major digital onboarding solution that enhances the process’s efficiency and organization. It enables the storage, organization, retrieval, and sharing of digital documents in a centralized electronic repository. Documents are typically scanned or uploaded into the system, where they can be indexed, tagged, and categorized for easy searching and retrieval.

Check out the list of some best Document Management Software.

Pros

Cons

Pros

- Digital document management systems allow lenders to store, manage, and retrieve customer documents electronically and securely.

- It eliminates the need for physical storage, reduces paperwork, and enables efficient document sharing and collaboration.

Cons

- Implementing a digital document management system may require an initial investment in technology infrastructure and staff training.

- Effectiveness of proper data encryption and security measures to protect sensitive customer information is still in doubt among customers.

Digital Onboarding Platforms

Digital onboarding platforms provide a user-friendly interface for individuals to submit their applications electronically. Users can access the platform via a web or mobile application, input their personal information, and provide necessary documents. The platform may include features such as form validation, document upload capabilities, and real-time feedback to guide users through the application process.

Click here to learn more about the top Digital Onboarding Software Platforms.

Pros

Cons

Pros

- Offer convenience, faster processing, and an improved user experience.

- Reduce costs, improve data accuracy, and enable seamless integration with other systems, resulting in greater efficiency and a streamlined application process.

Cons

- Need for reliable internet connectivity, possible technical issues or system downtime that may disrupt the application process.

- The possibility of user unfamiliarity or resistance to digital platforms, which could affect adoption rates.

Customer Relationship Management (CRM) Systems

In the digital onboarding journey, a CRM system can capture, organize, and leverage customer information to enhance the onboarding process. A CRM system integrates various touchpoints and channels to collect customer data, including contact details, preferences, communication history, and interactions. This data is then stored, organized, and made accessible to relevant stakeholders involved in the onboarding process. It is a centralized hub for customer information, facilitating effective communication, task management, and data-driven decision-making in the digital onboarding journey.

Here is a curated list of the best CRM Software solutions.

Pros

Cons

Pros

Using CRM systems, lenders can effectively manage customer interactions, streamline the onboarding process, improve customer communication, and foster long-term customer relationships beyond the initial onboarding stage.

Cons

- Implementing a CRM system in the customer onboarding journey can come with the drawback of requiring upfront investment and staff training. This initial cost and time investment may pose a challenge for lending institutions.

- Selecting a CRM solution that precisely aligns with the specific needs and scale of the lending institution is crucial. Failure to choose the right CRM system may lead to inefficiencies

Striking a Balance: Choosing the Right One

A great customer onboarding experience has the power to increase conversions, improve banks’ reputations, and boost efficiencies. While each solution offers unique advantages, it is crucial for lenders to carefully evaluate their specific needs, budget, and customer expectations before selecting the most suitable option.

Let’s check out the factors to consider:

Compliance and Regulatory Requirements: Ensure the solution meets the necessary compliance and regulatory standards, such as KYC (Know Your Customer) and AML (Anti-Money Laundering) regulations.

Scalability and Flexibility: Evaluate the solution’s ability to scale and adapt to the organization’s growing needs and changing requirements.

Integration Capabilities: Consider the solution’s compatibility with existing systems and technologies.

User Experience: A smooth and efficient onboarding process can enhance customer satisfaction and drive engagement.

Security and Data Privacy: Ensure the solution offers robust security measures to protect sensitive customer data.

Analytics and Reporting: The solution should provide valuable insights and generate comprehensive reports on customer onboarding metrics, allowing for data-driven decision-making and continuous improvement.

Cost and Return on Investment (ROI): Evaluate the potential ROI by assessing the solution’s ability to streamline processes, reduce manual efforts, and improve efficiency.

With the right onboarding solution, firms can experience several immediate benefits, including improved completion rates, reduced callbacks, minimized compliance issues, and enhanced customer experience.

Embracing digital onboarding solutions is no longer a luxury but a necessity for lenders looking to stay competitive and deliver exceptional customer experiences in today’s digital age.

Boost Member Retention, Fuel Credit Union Growth

How can we ensure your credit union’s success in today’s competitive landscape? The answer lies in a simple yet critical question: How effective is your member retention strategy? Why is retaining customers so important? Well, it’s simple. Retaining your existing members is more cost-effective than acquiring new ones. Member Retention: The Key to Sustainable… Continue reading Boost Member Retention, Fuel Credit Union Growth

Regulatory compliance is a big deal in the lending business. It’s not something you can afford to ignore or take lightly. Following the rules and regulations set by the authorities is crucial for lending institutions to stay out of trouble and keep their operations running smoothly. Operating in a non-compliant manner can face hefty fines, legal concerns, and damage to your reputation that might be hard to recover from.

In recent years, financial institutions have faced billions of dollars in fines due to non-compliance with lending regulations. Yep, you heard it right—billions! That’s a staggering amount that could seriously dent your bottom line and put your business in jeopardy. It’s not just about playing by the rules; it’s about protecting your business and setting yourself up for long-term success.

Lenders battle compliance complexity

Lenders face significant challenges in the compliance landscape due to the complex and evolving regulatory environment. Firstly, the sheer volume and complexity of regulations can be overwhelming for lenders to navigate. They must keep up with many rules and requirements, often varying across jurisdictions, increasing compliance efforts’ complexity. Additionally, regulatory agencies frequently introduce new regulations or update existing ones, making it challenging for lenders to stay current and ensure compliance. Lenders must also invest in robust compliance systems and technologies to monitor and track compliance activities effectively. Moreover, the risk of non-compliance penalties, fines, and reputational damage adds to lenders’ pressure.

The potential costs of non-compliance are staggering and extend far beyond simple fines. Organizations lose an average of $5.87 Million in revenue due to a single non-compliance event.

Here are some recent and shocking data points to consider:

- In 2020 alone, banks were fined $14.2 Billion for non-compliance, with the United States accounting for 78% of issued fines.

- JP Morgan was fined $125 million in 2021 for failing to implement compliance controls.

Compliance efforts often require dedicated teams, resources, and ongoing training to ensure adherence to regulations. Overall, lenders must continually adapt to the changing compliance landscape, stay ahead of regulatory changes, and invest in compliance infrastructure to mitigate risks and maintain regulatory compliance.

Lenders non-compliance fallout

Unveiling the aftermath of non-compliance, lenders face the daunting fallout that reverberates through their operations and reputation.

- Financial penalties and fines imposed by regulatory authorities for non-compliance

- Potential suspension or revocation of the firm’s license to operate.

- Strained relationships with loan providers due to loss of trust and hesitancy to provide further funding.

- Limited access to financing and credit facilities hinders the firm’s growth plans.

- Adverse publicity and damage to the firm’s reputation

- Erosion of customer trust and confidence, leading to a loss of clients and business

- Rebuilding a tarnished reputation requires significant resources and time.

Mitigating Regulatory Compliance Risks: Essential Steps for Operational Resilience

In the dynamic landscape of complex regulations, gaining a profound comprehension of compliance risks is paramount. By stepping back and assessing vulnerabilities within your loan cycle you can effectively mitigate these risks and navigate the complexities of the regulatory environment.

Let us dive in and conquer regulatory compliance together!

- Robust Compliance Framework: Establish a comprehensive compliance framework that includes policies, procedures, and controls to ensure adherence to regulatory requirements.

- Regular Risk Assessments: Conduct regular risk assessments to identify and mitigate compliance risks specific to your organization. Stay updated on industry trends and regulatory changes that may impact your operations.

- Technology Adoption: Invest in compliance-focused technology solutions such as automated monitoring systems, data analytics tools, and risk management software to enhance efficiency and accuracy in compliance processes.

- Compliance Monitoring and Reporting: Implement robust monitoring mechanisms to identify and address compliance issues proactively. Maintain accurate records and generate timely reports to demonstrate compliance with regulatory authorities.

- Regular Compliance Reviews: Conduct periodic reviews and assessments of your compliance program to identify gaps or areas that need enhancement and implement necessary adjustments.

How can Insight Consultants help?

Building an effective compliance strategy is crucial and can be a big lift for firms. At Insight, we are flexible in supporting your compliance responsibilities.

We offer:

- Automate and customize adverse action notices, ensuring adherence to regulatory requirements while streamlining the process and improving consumer communication efficiency.

- Generate personalized notices tailored to individual consumers, reducing errors and enhancing communication effectiveness.

- Support multiple versions of customizable notices, accommodating diverse variations and specific requirements, providing the necessary flexibility in the notification process.

- Automated email, text, and on-screen notifications to ensure the generation of disclosures within the specified time frame, promoting timely delivery and compliance.

- Additional automated email, text, and on-screen notifications to ensure that applications are decisioned following your institution’s service levels.

- We have established systems and procedures to effectively handle data collection, testing, and compliance requirements associated with regulations such as HMDA, CIP, MLA, HPML, HCML, ATR, and QM.

- Text /email alert system to notify users of any changes in loan status, including loan declines, withdrawals, or other updates.

With the ever-changing regulatory landscape, lending firms are presented with a prime opportunity to use technology to proactively reshape their compliance function. By strategically modifying their operating model and processes, they can elevate the quality of oversight and drive operational efficiency. Embracing this transformative journey equips lending firms with a competitive edge, allowing them to deliver exceptional service, optimize costs, and effectively manage operational risks.

If you want to learn more about our compliance management services, contact us here.

Get Insights to stay ahead in the Lending Industry.

Insights delivered monthly!

Credit risk management is a crucial aspect of financial management that involves identifying, evaluating, and mitigating the potential risks when lending money to borrowers. With the ever-changing economic landscape, it has become increasingly important for financial institutions and businesses to have a robust credit risk management framework.

To address these opposing needs, Insight Consultants offers a few tips to optimize credit management to enhance business performance. These tips empower lenders to accelerate credit origination, customize credit lines, track global business exposures in real time, and mitigate business risks.

Significant Challenges in Credit Risk Management

Lending firms are under significant pressure to transform their credit management business. There is a paradigm shift in how they conduct business operations, giving rise to new challenges in credit management.

In the race to implement risk strategies to improve overall performance and secure a competitive advantage, firms must overcome significant credit risk management challenges, such as:

- Inefficient Data Management: Organizations struggle to manage the vast amounts of data involved in credit risk management, leading to inconsistencies, errors, and redundancies.

- Ineffective Risk Management: Credit risk management is a complex process that demands a comprehensive and systematic approach. However, some firms may encounter difficulties implementing a practical risk management framework, leading to inadequate risk management practices.

- Complex Regulatory Requirements: Lenders face pressure to comply with complex regulatory requirements. Fulfilling these requirements can be time-consuming and costly.

- Cumbersome Reporting: Inefficient data management systems can contribute to the challenge of cumbersome reporting, with data silos and disparate systems making it challenging to access and compile necessary data.

Quick Steps to Optimize Credit Management

As vulnerability to credit continues to be the primary risk factor for the financial industry worldwide, lenders should take special initiatives in strategizing comprehensive measures to identify, monitor, and control the inherent risks in lending as effectively as possible.

To address these competing needs, Insight Consultants offers a few tips to optimize credit management to enhance business performance. These tips enable lenders to accelerate credit origination and customize credit lines while tracking global business exposures in real-time and mitigating business risks.

1. Leverage Automation: Manual data entry is bound to lead to inconsistencies, errors, or redundancies. Replacing manual entries with automated entries can ensure that data is added and shared correctly throughout your organization. Automation can reduce costs, increase efficiency, and improve data accuracy.

Insight Consultants solution: By automating processes like customer onboarding, underwriting, and credit scoring, our solutions help lenders streamline operations and improve risk management.

- Faster customer onboarding: Digital onboarding replaces a paper-intensive credit management process with an electronic one to enable better credit portfolio and risk management and faster onboarding of new customers.

- Automated underwriting: Using machine learning algorithms and other digital tools to automatically underwrite loans can help reduce the time and resources required for manual underwriting.

- Eliminate manual credit scoring: By using credit data and pre-written algorithms, risk scores, categories, and credit limits can be automatically assigned, saving time and effort for analysts.

- Real-time credit risk monitoring: Implementing a visible and transparent system and introducing reports and analytics enables the C-suit to monitor the process effectively.

2. Proactive risk assessmentProactive credit risk management improves an organization’s ability in effective decision-making. It helps build an understanding required to measure and manage emerging risks, giving organizations a better view of tomorrow’s risk and how it impacts their business. Predictive analytics can enable organizations to identify proactively.

Insight Consultants Solution: Our credit scoring model assists lenders in evaluating the creditworthiness of borrowers, determining the level of risk associated with lending to them, and making informed decisions about extending credit. These models provide early warning systems by analyzing historical data and detecting patterns that indicate potential future issues. The models can generate alerts or notifications, allowing timely intervention to mitigate or prevent adverse outcomes.

3. Digitization of Business Processes The lending sector’s ever-changing, heavily regulated, and competitive landscape requires highly flexible solutions. It will give organizations the operational agility to achieve business objectives and ensure regulatory compliance. The digital transformation of existing credit risk tools, processes, and systems can address rising costs, regulatory complexity, and new customer preferences. Digital solutions can also enable organizations to make more informed lending decisions and minimize credit risk.

Insight Consultants Solution:

- Digitizing the credit application process: It involves an online form submission, secure data analysis, creditworthiness assessment, electronic notification, digital loan agreement signing, and fund transfer. Streamlining the application process through digitization can make it more efficient. This can also allow for real-time validation of applicant data.

- Digital document management: It involves converting paper-based documents into electronic formats, categorizing them into folders or databases, applying metadata and tags to make them easily searchable, and setting up user access controls to ensure security and privacy. Digitizing the document management process can help improve loan origination efficiency and reduce errors and delays associated with paper-based processes.

- Electronic signatures: Digital signatures can streamline credit management by simplifying the credit application process, reducing paperwork, and increasing security and compliance. Using digital signatures allows credit applications and loan agreements to be signed electronically, allowing faster processing times and reducing the risk of errors or missing documents.

4. Use of effective tools and technologies: When keeping track of all the variables contributing to a customer’s creditworthiness and risk, employing the right tools & technology is critical. Advanced analytics and AI (Artificial Intelligence) can enable organizations to assess credit risk, identify potential fraud, and improve overall risk management more accurately.

When keeping track of all the variables contributing to a customer’s creditworthiness and risk, employing the right tools & technology is critical. Advanced analytics and AI (Artificial Intelligence) can enable organizations to assess credit risk, identify potential fraud, and improve overall risk management more accurately.

In addition to the tips listed above, it is essential to emphasize the importance of collaboration between stakeholders such as credit risk analysts, compliance officers, and business leaders. These groups can ensure that credit risk is accurately assessed and managed. Furthermore, macroeconomic factors like interest rates and inflation can significantly impact credit risk management. Understanding how these factors can influence credit risk can help organizations better prepare for potential changes in the economic landscape.

Key business benefits

Many lenders focus more on sales and tend to neglect credit management. However, it is prudent to note that lending firms are particularly vulnerable to unpaid debts and overdue customer payments. By implementing robust credit screening processes, monitoring borrowers’ creditworthiness, and establishing clear credit terms, lenders can mitigate risk, improve cash flow, and increase profitability. Managing credit optimally is crucial to your business’s growth and survival.

Benefits:

- Make consistent, informed credit decisions.

- Improved cash flow

- Enhanced customer relationships

- Increased profitability and reduced terrible debts.

Conclusion

Insight Consultants prioritize customer experience and operational excellence to ensure that the customers enjoy their interactions with the lenders across their journey. We have proven methodologies and experience to achieve measurable and sustainable results while mitigating risk. We aim to help our clients make the right investment decisions for dollars and effort.

Lenders should be geared to addressing two facets of credit management: Customer’s unique facing needs and business profitability and risks. Insight Consultants help their clients to address these opposing needs. Our solution allows lenders to accelerate credit origination and customize credit lines while tracking global business exposures in real-time and mitigating business risks.

With global lending subject-matter expertise, cross-disciplinary service offerings, and insight into solution options complemented by solid vendor relationships, our Business Consulting and Technology teams have the necessary experience and knowledge to guide lenders through their credit management journey.

Trends in Digitization: Credit Unions Revolutionize Operations for a Tech Savvy Word

In today’s tech-savvy world, where customers expect seamless digital experiences, credit unions must revolutionize their operations to stay competitive. Credit unions must adopt digital technologies to remain competitive and provide efficiency in operations. The digital transformation of credit unions is a strategic imperative for long-term success. By embracing digital technologies, credit unions can stay relevant… Continue reading Trends in Digitization: Credit Unions Revolutionize Operations for a Tech Savvy Word